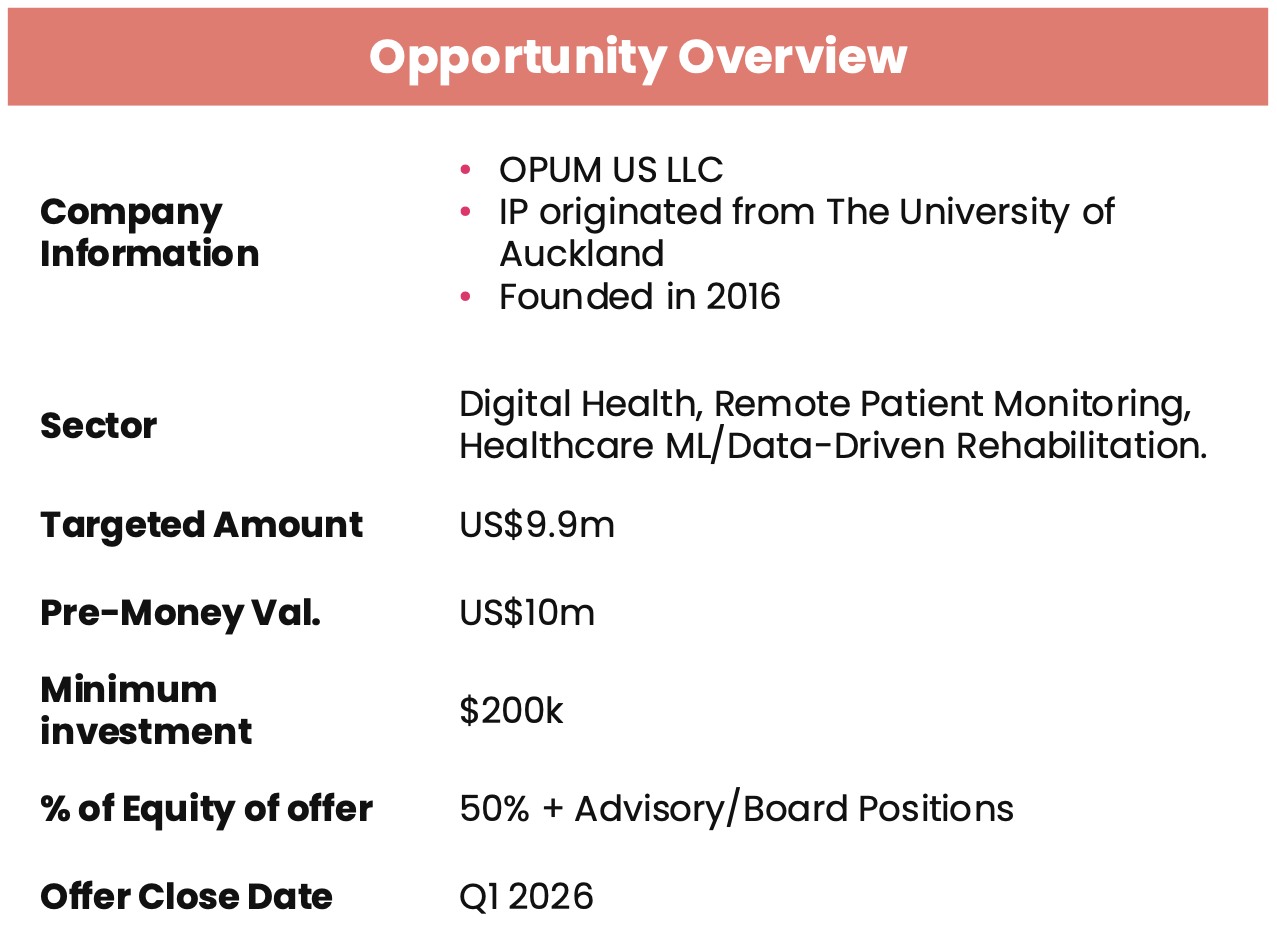

Investment Summary

OPUM Technologies

Reinventing Recovery: A Digital Platform for Musculoskeletal Health

Overview:

OPUM Technologies is transforming musculoskeletal rehabilitation by integrating patented wearable sensors, real-time data, and AI-driven insights into a seamless digital health platform.

OPUM is a US-based digital health company leveraging its patented "Digital Knee®" sensor, a HIPAA-compliant patient monitoring ecosystem, and AI-enabled clinician tools to modernize orthopedic recovery.

This intelligent RTM-enabled platform streamlines rehab, verifies compliance for insurers, and empowers patients—unlocking scalable efficiency for clinics and payers.

OPUM aims to become the "Fitbit of Joint Recovery"—delivering real-world outcomes and reimbursement validation at population scale. Investors participate through a common equity raise designed to offer equity upside in a $4B+ addressable market.

This offering is ideal for investors seeking exposure to digital health, value-based care, and medical device innovation—without the timeline risks of biotech or pharma.

Why This Equity Round?

A Hybrid Structure with Proven Technology and Market Fit

Key features of this offering include:

• $10M Pre-Money Valuation, $9.9M Raise, 50% Equity Offered

Poised for rapid value appreciation based on clinical traction, IP position, and payer demand.

• Patented Digital Health IP

Exclusive technology developed at the University of Auckland—addressing both patient outcomes and insurer requirements.

• SaaS-Enabled Recurring Revenue

Monthly reimbursement revenue above 80%.

• Validated Market Demand

Pilot programs, payer interest, and FDA cleared technology position OPUM for accelerated rollout.

Why Musculoskeletal Health?

“The Ultimate Value-Based Health Market”

• 1 in 4 adults in the U.S. suffer from joint issues

• ACL, TKA, and OA cases exceed 2.9M annually—$1B+ addressable market for knee conditions alone

• Rehab adherence is <50%—wasting surgeries, slowing healing, and frustrating payers

Driven by:

• Increasing volume of surgeries (ACL/TKA projected to double by 2030)

• Stricter insurance reimbursement criteria (Medicare now requires documented pre-surgery rehab)

• Push toward remote care and digital patient engagement

• High cost of re-injury and revision surgeries

Access has historically been fragmented and analog—until now.

Platform Strategy: Diversification Across Joint Care

Capital from this round will support a revenue-diverse strategy:

• Smart Braces (OPUM Stock): Turnkey rehab tech with embedded sensor for clinic-scale deployment

• Custom Solutions (OPUM Custom): Sensor retrofit for surgeons/PTs using third-party braces

• Remote Monitoring SaaS: Monthly per-patient RTM reimbursements with full clinician oversight

• Data Monetization: Aggregated biomechanical insights for payers and insurance validation

• Expansion into Other Joints: Hips, shoulders, elbows, and wrists

Proven Leadership: A Team Built for Execution

• David Smith, CEO: Founded and sold Tenaxis Medical for $168M

• James Henderson, Chair: 30+ years in capital markets, healthcare leadership

• Alexandra Wilson, VP Finance & Administration: Scaled consumer brands and guided OPUM through receivership to commercialization

• Daniel Willis & Edward Chen, Software Leads: Built and scaled OPUM’s HIPAA-grade platform

• Cody Wilson, Product Manager: Ex-Smith+Nephew and founder of AI health tech platform TrialIQ

We don’t just have product-market fit—we have operational firepower to scale.

Investment Structure: Designed for Growth and Exit

| Feature | Investor Benefit |

|---|---|

| $10M Pre-Money Valuation | Entry at compelling discount to market size |

| 50% Equity Offered | Significant ownership in a growth-stage firm |

| Target Raise: $9.9M | Funds 24-month runway to EBITDA+ |

| Revenue by 2028: $41.4M | Driven by high-margin products + SaaS |

| Exit Timeline: 3-5 Years | IPO or strategic acquisition pathway |

| IP Ownership: 100% | Exclusive patents from Univ. of Auckland |

Conclusion: The Future of Recovery Is Here

OPUM Technologies’ common equity isn’t just an investment—it’s a stake in the future of orthopedic care.

By combining hardware, software, and SaaS in one seamless platform, we give investors access to:

• A $1B+ wedge in the $4B joint rehab market

• A patented platform built for RTM reimbursement and clinical compliance

• A management team with exits and operational track records

• A vision that expands across joints, data monetization, and sports medicine

OPUM is where better care meets better outcomes—and scalable revenue.

{kind=link}