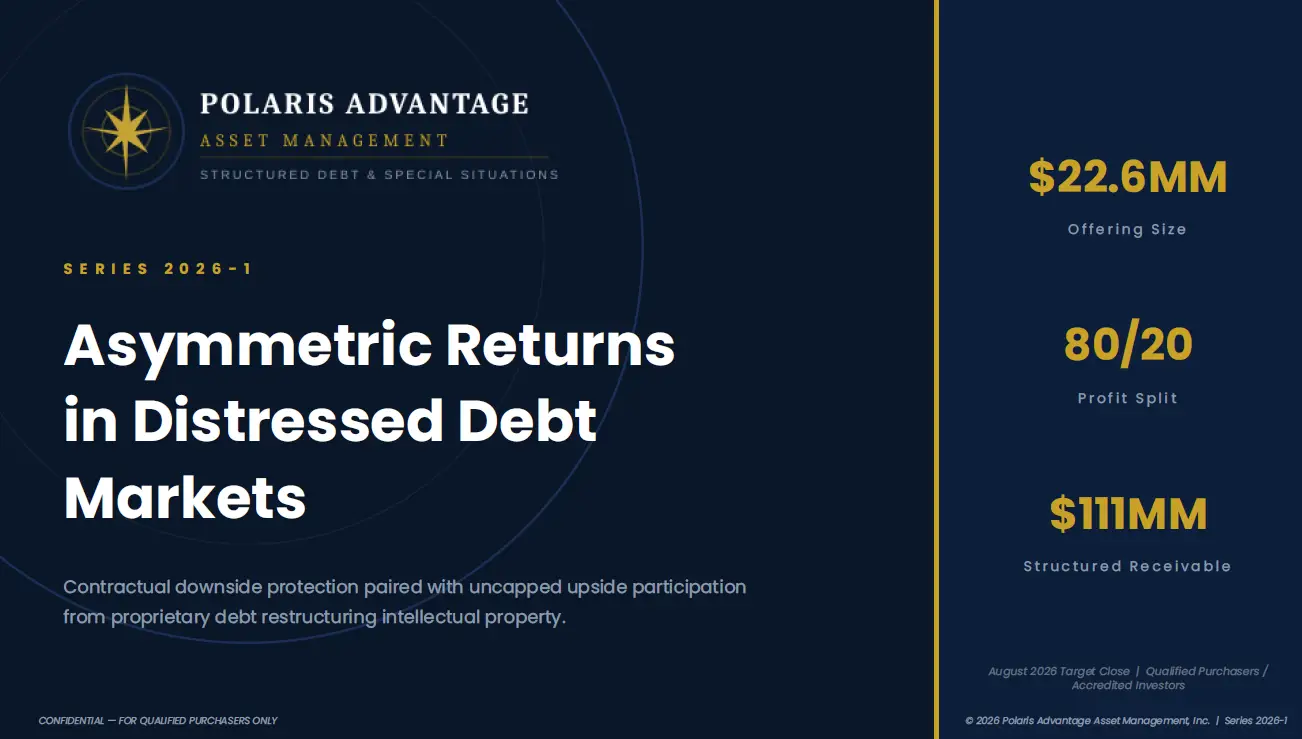

A Unique Value Proposition in the Debt Markets

The Polaris Advantage Issuing Trust (the “Trust”) is a purpose-built vehicle providing qualified investors differentiated exposure to a curated portfolio of bonds and debt instruments undergoing restructuring. The Trust’s strategy is powered by proprietary, debt-related intellectual property — a library of structuring, claimsenhancement, and workout methodologies designed to position the Trust to realize potential restructuring proceeds in excess of stated face value. The structure pairs this asymmetric upside participation with contractually-supported downside protection — a combination not typically available to institutional debt investors.

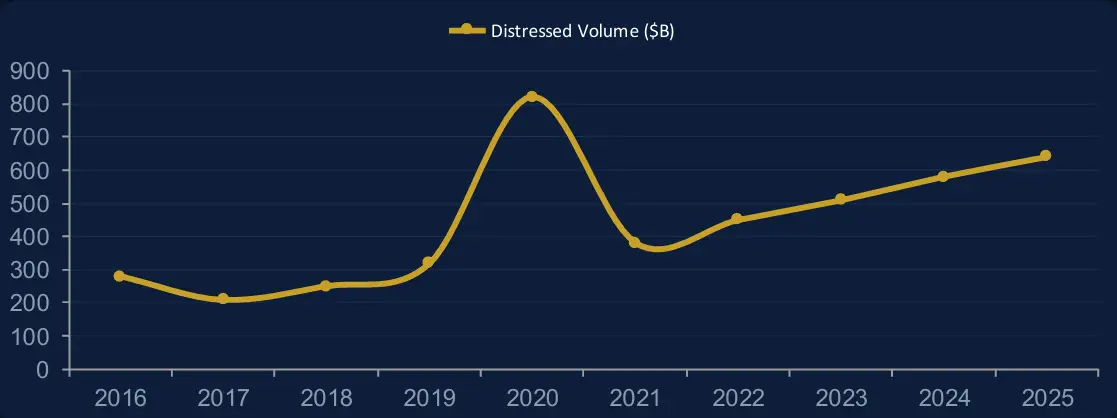

Market Inefficiency

Distressed debt markets exhibit persistent mispricing. Traditional institutional buyers lack the proprietary restructuring IP to unlock value embedded in complex debt instruments trading below recovery value.

Asymmetric Structure

The Trust captures upside through an 80/20 profit split on returns above par recovery while an $111MM structured receivable provides a contractual par-floor — a combination rarely available to institutional debt investors.

Proprietary Edge

A library of structuring, claims-enhancement, and workout methodologies developed over years of institutional credit practice positions the Trust to extract value inaccessible to conventional market participants.